Is Loudoun County Still a Good Place to Buy in 2026?

A practical, data-backed look at today's market

If you’ve been considering buying a home in Loudoun County, VA, you’ve probably asked yourself some version of this question:

Does buying even make sense right now?

Between higher mortgage rates and home prices that never really came down, the decision feels a lot less straightforward than it did a few years ago.

The short answer:

It depends, but the market isn’t as irrational as it might feel.

Let’s break it down below:

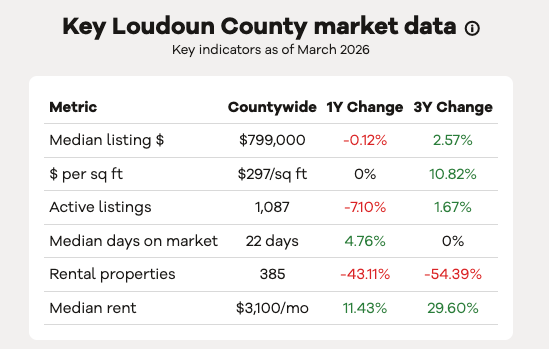

A Quick Snapshot of the Loudoun Market

The Loudoun County housing market in 2026 looks very different from the frenzy of 2021-2022, but it’s also far from a downturn.

What This Data Tells Us

At a high level, this is a market that’s holding steady, not declining.

Home prices have effectively plateaued over the past year, but when you zoom out, values are still higher than they were just a few years ago. That suggests we’re not seeing price correction so much as a pause after rapid growth.

At the same time, inventory has actually declined year-over-year, which helps explain why prices haven’t softened. Even with slightly longer days on market, supply still isn’t high enough to put downward pressure on pricing.

What About Renting?

The most notable shift in the housing data is on the rental side. With rents up double digits and rental inventory sharply down, the cost (and availability) of renting has become a much bigger factor in the rent vs. buy decision. Waiting to buy doesn’t necessarily mean locking in a cheaper monthly payment, it may just mean paying more in rent while you wait.

The Rent vs. Buy Reality in 2026

In many cases today, owning costs more month-to-month than renting.

This is largely due to mortgage rates still being elevated compared to the ultra-low rates we saw a few years ago.

With median rents around $3,100/month, a comparable home purchase, at today’s prices and mortgage rates, will often result in a higher monthly payment, especially once taxes and insurance are factored in.

What we know:

Rent is rising quickly (+11.4% YoY)

Rental options are shrinking significantly (-43% inventory YoY)

Home prices are holding steady, not declining.

Buying today is less about immediate savings and more about:

Locking in a fixed housing cost (as far as P&I goes)

Building equity over time

Avoiding continued rent increases

Comparing Renting and Ownership at Today’s Prices

With the average monthly rent of $3,100 and average home price of $799k, let’s compare what you get for that if you were to rent vs. buy.

Scenario 1: Renting

Address: 25274 Gothic Sq, Chantilly, VA 20152

Monthly Rent: $3,100

Square Feet: 2,456

Cost PSF: $1.26

Upfront Cost: Security deposit (could be 1-month rent) & application fees

Flexibility: High

Equity: None

Scenario 2: Buying at Median Price (~$799k)

Address: 429 Deerpath Ave SW, Leesburg, VA 20175

Purchase Price: $799,500

Square Feet: 3,263

Cost PSF: $245

Interest Rate: 6.43% (varies by buyer)

Down Payment: 20% ($159,900)

Monthly Cost: 4,013.31 (Principal & Interest); $4,550 (incl. Taxes and Insurance)

Upfront Cost: Down payment + closing costs of ~2-5%

Flexibility: Low

At first glance, renting appears significantly more affordable than buying. A median rent of around $3,100 per month is well below the monthly cost of purchasing a home at the county’s median list price of $799k.

But it’s not an apples-to-apples comparison.

In today’s market, most rental options around the $3,100 price point tend to be townhomes. Conversely, a purchase price near $799k often puts buyers in range of a single-family home, depending on location and condition.

When doing a search for comparable townhomes, however, the prices were largely near $725k - $750k, so not far below the median list price. Purchasing a $750k townhome with 20% down at 6.43% yields a monthly payment of $3,765 before taxes and insurance, and ~$4,300 with.

It’s important to keep in mind the rent vs. buy decision isn’t only about monthly payment, it’s also about space, privacy, and long-term needs.

Scenario 3: Buying a Home and Paying the Median Rent Amount

So you want to buy but you don’t want to spend more than the median rent on PITI (Principal, Interest, Taxes, Insurance)? Let’s look at that.

The numbers primarily differ depending on your down payment, so we will look at this at different levels.

Max Monthly PITI: $3,100

Interest Rate: 6.43%

Loan Term: 30-yr fixed

If you put down ________, you can afford a home worth up to __________.

1. $25,000; $406,000

2. $75,000; $472,000

3. $100,000; $519,000

4. $150,000; $588,000

5. $200,000; $638,000

6. $300,000; $738,000

7. $365,000; $802,600

If you want to exclude Taxes and Insurance and just cover Principal and Interest in the $3,100, it would still take a down payment of $300,000 to afford a home of $794,000.

As you can see, matching today’s median rent with a home purchase would require a much larger upfront investment/down payment than many buyers are planning for.

Otherwise, you’d need a significantly lower purchase price or lower interest rate to be able to match rent.

Who Buying Still Makes Sense For?

Even in today’s market, there are clear scenarios where buying in Loudoun County, VA is still a strong decision.

You plan to stay for 5+ years

With modest appreciation projected, time in the market matters more than timing the market. A longer horizon allows you to ride out short-term fluctuations and benefit from gradual appreciation.

Your income is stable and you’re not stretching

With median home prices around $799k, this isn’t a market that favors stretching. Buyers who are financially comfortable have more flexibility to handle higher monthly payments and unexpected costs.

You want payment stability

Fixed housing costs and control over your space still matter, especially in a rising rent environment.

Who May Want to Wait to Buy?

There are also situations where holding off is the more practical choice.

You Have Short-Term Plans (under 3-5 years)

Transaction costs alone can outweigh any short-term appreciation.

You’re relying on rates dropping significantly

Rates may come down, but there’s no guarantee, and lower rates could bring more competition back into the market.

You’re highly payment-sensitive

If the difference between renting ($3,100/month) and owning is a stretch, waiting may provide more flexibility, especially as inventory and market conditions continue to evolve.

What’s Actually Changing in Loudoun County?

The underlying story for Loudoun County in 2026 isn’t volatility, it’s rebalancing.

Home prices are flat YoY

Inventory is still constrained, even after the peak frenzy years

Home are taking slightly longer to sell, giving buyers a little more breathing room

Rental pressure is increasing, not easing

Buyers have more time and less competition than before, but not enough supply to drive down prices.

What About You?

What would make buying feel “worth it” to you in today’s market? Please share in the comments!